North Adams City Council Sets Fiscal 2024 Tax Rate

NORTH ADAMS, Mass. — The average residential property tax bill will go up by $103.85 for fiscal year 2024 under a tax distribution plan OK'd by the City Council on Tuesday.

On a vote of 6-2, the eight members in attendance chose to follow the path recommended by the Board of Assessors and use a 1.715 shift differential from the residential to the commercial class of real estate.

That is the same differential the council authorized last year for FY23 after lengthy debate that stretched over two meetings and a 5-4 vote.

This time around, Councilors Marie T. Harpin and Peter Oleskiewicz, who voted in the minority a year ago, joined four of the councilors who approved the shift at last November's tax classification hearing.

Jennifer Barbeau and Wayne Wilkinson each voted against the 1.715 shift. Councilor Michael Obasohan did not attend the meeting.

Prior to the vote, Wilkinson moved that instead of the 1.715 shift favored by the administration, the council should set the shift at 1.70, which would have translated to an average residential tax bill rise of $122.47, according to the data supplied by Assessor Jessica Lincourt.

His motion did not receive a second.

While the overwhelming majority of residential property owners will see an increase in their tax bills in FY24, the city's tax rate actually is going down for both commercial and residential properties.

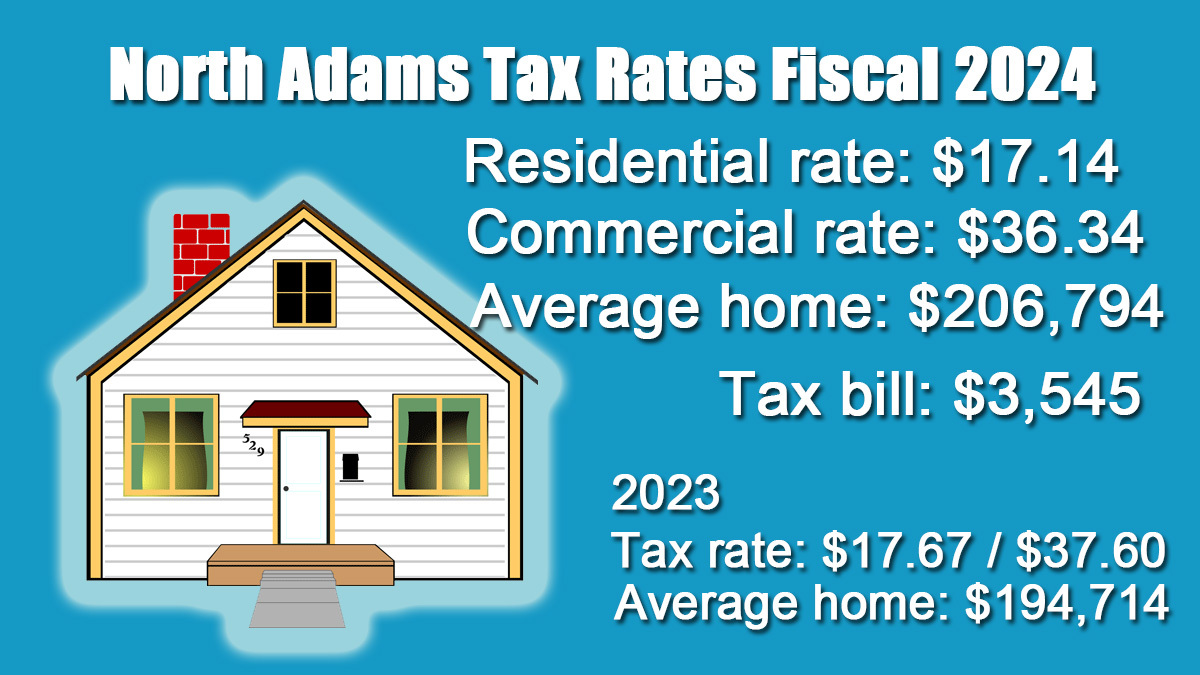

The residential and open space tax rate for FY23 was $17.67 per $1,000 of valuation. For FY24, that rate dips to $17.14. For commercial properties, the FY23 rate was $37.60.

The reason tax bills will go up while the tax rate falls is increased property values.

The average value of an averagle single-family residence in North Adams in FY23 was $194,713.98. In FY24, that number is $206,794.28, an increase of $12,080.30, or 6.2 percent.

The total value of the town's residential class rose by 6.9 percent, or $51.6 million, to $794.8 million. The commercial class saw a more modest increase of 3.6 percent, from $118 million to $122.4 million.

Factoring in the smaller industrial and personal property classes, the city's total valuation for FY24 tops $1 billion — $1.007 billion, versus $944.7 million in FY23.

The average commercial property in town is valued at $445,502 in FY24, up from $434,118 a year ago, an increase of $11,384 or 2.6 percent.

The tax bill on that hypothetical "average" commercial property was $16,322.86 in FY23 and will be $16,189.57 once Tuesday evening's vote is forwarded to the Department of Revenue, which then certifies municipal property tax rates. Had the council gone with Wilkinson's motion, the average commercial bill would have gone from $16,322.86 in FY23 to $16,047.01 in FY24.

Lincourt explained that municipal assessors follow Massachusetts law when reassessing properties.

"Assessors are required to assess all real and personal property at its fair cash value as of Jan. 1 each year," Lincourt said. "Fair cash value means fair market value, which is the price a willing buyer and willing seller would settle on in an open market transaction.

"To determine fair market value, assessors must evaluate a number of factors that impact the amount a willing buyer and willing seller would agree to, including sales, location and demand. In common terms … our property sales data is the primary reason for the increase and decrease in assessed values. If properties are routinely selling their assessed values, this indicates our assessed values should be increased to reflect the fair market value."

Lincourt noted that the Department of Revenue also reviews sales data at the local level to make sure municipalities are not overassessing or underassessing parcels.

"Some people think I just pull numbers out of the air," she said. "I do not."

In other business during the brief meeting, the council gave final approval to ordinance changes related to a hospital zoning overlay, taxis and recordation and publishing of ordinances on the city website; granting easements to Blackinton Mill LLC and Blackinton Backwoods LLC for access to the proposed North Adams Adventure Trail, and confirmation of the reappointment of Eric Wilson to the Commission on Disabilities for a term to expire Dec. 1, 2026.

Tags: fiscal 2024, tax classification,